The Side-Gig Tax Trap

Your SEP IRA Can Wreck Your Backdoor Roth

You are a high-earning professional. You max out your workplace 401(k) every year. You optimize your portfolio. And because your income phases you out of standard Roth IRA contributions, you use the Backdoor Roth strategy to get money into a tax-free growth bucket.

Then you start generating side-gig income.

Maybe you land a board seat, start consulting, or take on freelance fractional executive work. You have 1099 income now. You want to shelter it. A quick Google search, or a well-meaning but shortsighted CPA, points you to the SEP IRA.

It takes five minutes to open. The paperwork is minimal. And it lets you make a meaningful pre-tax retirement contribution on your self-employment earnings.

Then tax season arrives.

By funding that SEP IRA, you may have just contaminated your Backdoor Roth strategy. The IRS Pro-Rata Rule treats your SEP balance as part of your Traditional IRA pool, and that turns what should be a tax-free Roth conversion into a partially taxable event.

Part 1: The Example

Let's look at two years in the financial life of Marcus, a 45-year-old tech executive.

Marcus in 2024: Clean Setup

Marcus earns $250,000 at his W-2 job. His income is well over the IRS limit for direct Roth contributions, so he uses the Backdoor Roth:

Step 1: He makes a $7,000 non-deductible (after-tax) contribution to a Traditional IRA.

Step 2: Shortly after, he converts that $7,000 to a Roth IRA.

He has zero dollars in any other Traditional IRAs. The IRS views this as a clean conversion. He already paid income tax on that $7,000, so the conversion triggers $0 in new taxes. The money grows tax-free forever.

Marcus in 2025: The Mistake

Marcus has a great 2025. On top of his day job, he picks up a consulting gig that nets $100,000 in Schedule C profit.

To lower his tax bill, he opens a SEP IRA and funds it before December 31, 2025. The commonly cited SEP limit is "up to 25% of compensation," but for a self-employed person the IRS requires a calculation that adjusts for that SEP contribution itself and the self-employment tax deduction. The effective rate is roughly 20% of net self-employment earnings - on Marcus's $100,000 of net profit, that comes to about $19,700.

Later that same year, he executes his standard Backdoor Roth for 2025: he contributes $7,000 to his non-deductible Traditional IRA and converts it to Roth, expecting the usual $0 tax bill.

His CPA calls in early 2026 with bad news: the conversion wasn't tax-free. He owes ordinary income tax on most of it.

Marcus doesn't understand. He used after-tax money for the $7,000. How can they tax him again?

The Pro-Rata Rule.

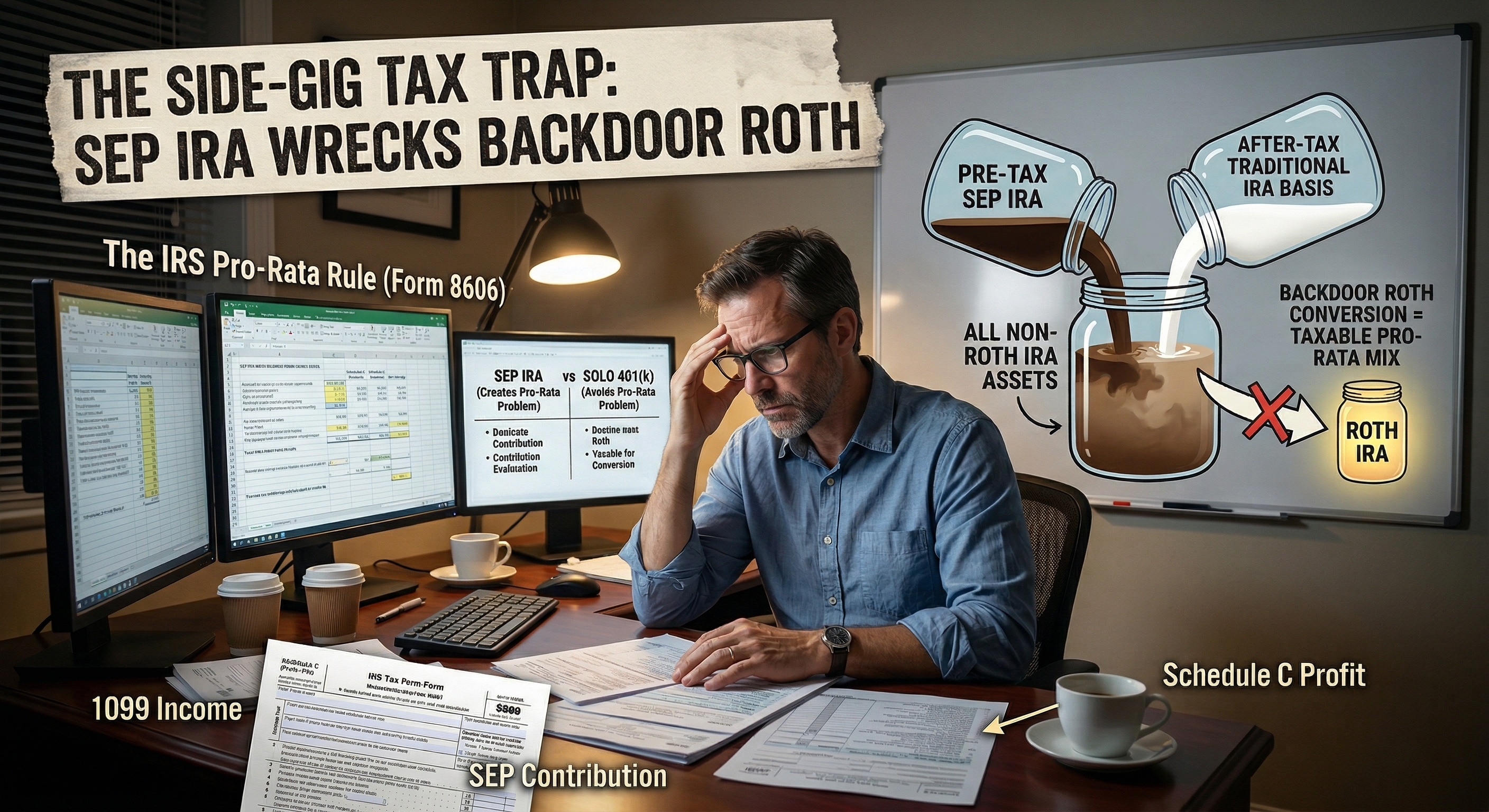

Part 2: The Pro-Rata Rule

The Backdoor Roth only works cleanly if you have no pre-tax money in any traditional, SEP, or SIMPLE IRA on December 31 of the conversion year.

When you convert money from a Traditional IRA to a Roth IRA, the IRS doesn't let you cherry-pick which dollars you're converting. The Pro-Rata Rule, applied through Form 8606, forces every conversion to be calculated proportionally across all your IRA assets.

Think of it like coffee and cream. Pre-tax dollars (never taxed) are coffee. Non-deductible, after-tax dollars are cream. Once they're in the same cup, they mix permanently. You can't take a sip and extract only the cream.

The IRS views all of your non-Roth IRAs as one single cup. Traditional IRAs, SIMPLE IRAs, and your SEP IRA - all one bucket.

Marcus's Math

Form 8606 builds a denominator from your year-end Traditional IRA value plus any Roth conversions during the year (plus any non-conversion distributions). Because Marcus already converted the $7,000 out of his Traditional IRA during 2025, that money isn't sitting in a Traditional IRA on December 31. But it still counts in the denominator.

Year-end Traditional IRA value (the SEP): $19,700

Roth conversion amount: $7,000

Form 8606 denominator: $26,700

Non-deductible basis (after-tax money): $7,000

The tax-free percentage of his conversion: $7,000 / $26,700 = about 26%.

That means roughly 74% of his $7,000 conversion - about $5,200 - is taxable as ordinary income at his marginal rate.

Instead of a tax-free Roth conversion, Marcus owes tax on $5,200. And as long as that pre-tax SEP money remains in an IRA, future Backdoor Roth conversions will still keep being partially taxable every year.

This isn't necessarily permanent. Marcus can fix it by rolling the SEP IRA balance into a qualified employer plan (like his day job's 401(k) or a Solo 401(k)) if that plan accepts incoming IRA rollovers. Once the pre-tax IRA money is out of the IRA system, his Backdoor Roth is clean again. But it's a hassle he didn't need to create.

It's also worth noting: the SEP deduction still saved Marcus more in year one than the pro-rata tax cost him. He deducted $19,700 of income while only $5,200 of his conversion became taxable. Btu there remains ongoing friction - every future Backdoor Roth conversion stays partially taxable until he clears the pre-tax IRA balance.

A Timing Note

One detail that trips people up: a Traditional IRA contribution can be made for 2025 as late as April 15, 2026, but a Roth conversion is reported in the calendar year it actually occurs. If Marcus contributes for 2025 but waits until January 2026 to convert, that's a 2026 conversion, not a 2025 conversion. The timing of the conversion determines which year's Form 8606 applies.

Similarly, the SEP funding date matters. Form 8606 uses your December 31 IRA value for the conversion year. If Marcus had waited until early 2026 to fund his SEP (which is allowed since SEP contributions for 2025 can be made until the tax filing deadline), that money wouldn't show up in his December 31, 2025 IRA balance, and his 2025 Backdoor Roth conversion would have been clean. Of course, it would contaminate his 2026 conversion instead. The lesson: the calendar year you actually move money into the SEP is what matters, not the tax year the contribution is "for."

Part 3: The Fix - The Solo 401(k)

If you have W-2 income, 1099 side-gig income, and you rely on the Backdoor Roth, the SEP IRA creates a problem you don't need.

You need a vehicle that shelters your side-gig income without adding pre-tax money to your IRA pool.

That vehicle is the Solo 401(k), also called an Individual 401(k). One eligibility note: this plan is designed for a business owner with no employees other than a spouse. If your consulting business has employees, you'll need a different plan structure.

The tax code draws a hard line between IRAs and qualified employer plans like 401(k)s. The Pro-Rata Rule only applies to IRAs. Balances inside a 401(k) - your employer's plan or a Solo 401(k) you opened for your consulting business - are invisible to the Form 8606 calculation.

How This Saves Marcus

If Marcus had opened a Solo 401(k) instead of a SEP IRA:

He deposits his roughly $19,700 employer contribution into the Solo 401(k). Same tax deduction.

The Solo 401(k) sits outside the IRA system entirely.

On December 31st, the IRS looks at his IRA balances for Form 8606 purposes. Pre-tax IRA balance: $0.

His $7,000 Backdoor Roth conversion is 100% tax-free.

Same deduction. No Pro-Rata damage.

Solo 401(k) vs. SEP IRA on Contributions

In Marcus's case - already maxing out his employee deferral at his day job - the Solo 401(k) and SEP IRA have similar contribution room on the employer side. IRS rules require employee elective deferrals to be aggregated across all plans, so if Marcus already used his full $23,500 deferral at work, his Solo 401(k) generally only has employer profit-sharing room (roughly 20% of net self-employment earnings, same as the SEP).

Where the Solo 401(k) pulls ahead is for side-gig earners who don't have a W-2 employer plan, or haven't maxed out their employee deferral elsewhere. In those cases, the Solo 401(k) allows both employer profit-sharing and employee deferrals, which can increase the total contribution significantly.

Some Solo 401(k) providers also support plan documents that permit voluntary after-tax contributions. This opens the so-called "Mega-Backdoor Roth" - a way to funnel additional dollars into a Roth environment. A SEP IRA can't do this.

And some Solo 401(k) plans allow participant loans (typically up to $50,000 or 50% of the vested balance), though this depends on the plan document, and loans that don't meet repayment rules can become taxable deemed distributions.

The Bottom Line

The SEP IRA is simple - minimal paperwork, no plan document, no tax filing. A Solo 401(k) is more work. It requires an EIN, a plan document, and must be established by December 31 of the contribution year. Once plan assets exceed $250,000, you'll need to file Form 5500-EZ annually. But modern custodians like Schwab and Fidelity have streamlined most of this.

If you are a high earner who uses the Backdoor Roth, check your IRA accounts. If you have a side gig and no employees, the Solo 401(k) avoids creating new pre-tax IRA balances from the side gig - and that's valuable. If you already have pre-tax money in existing traditional, SEP, or SIMPLE IRAs from prior years, talk to your advisor about rolling those into an employer plan to get your IRA pool clean before your next conversion.

This article is provided for educational and informational purposes only and does not constitute investment advice, a recommendation, or an offer to buy or sell any securities. The information presented reflects general tax and investment planning principles and should not be construed as personalized advice tailored to your individual financial situation. This article does not establish an advisory relationship with ArcVest, LLC. Before making any tax or investment decisions, you should consult with qualified professionals who can assess your specific circumstances.