International Equities Belong in Your Portfolio

What percentage of your risk assets are invested in the US? If you are like most US investors, it is over 80%. If that's you, should consider now a good time to sell high in the US and buy low elsewhere.

The U.S. represents roughly 60% of global equity market cap. Most domestic investors sit far above that level. This "home bias" feels safe because it's familiar, but it is a risk you aren't getting paid to take. Fixing it is simple: add Europe.

We’ve Seen This Movie Before

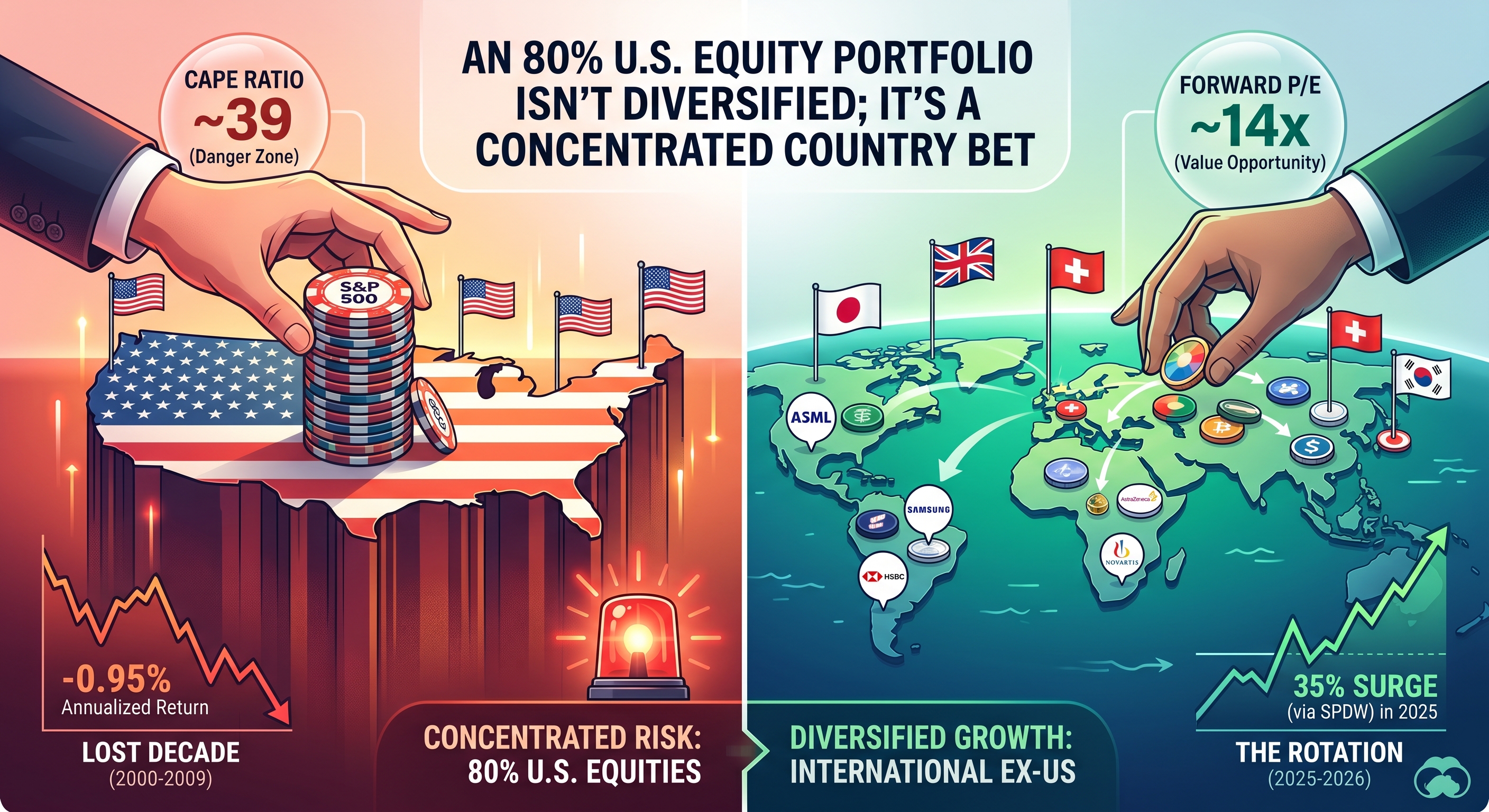

From 2000 through 2009 - the "lost decade" - the S&P 500 delivered an annualized return of -0.95%. A dollar invested on New Year’s Day 2000 was worth 91 cents ten years later.

Meanwhile, international developed markets (MSCI World ex USA) returned +1.6% annually, and emerging markets returned +9.8%. Diversified portfolios didn't just survive; they grew. The setup then was identical to the setup now: extreme U.S. valuations, narrow leadership, and a consensus that America was the only game in town.

The Valuation Gap is the Widest in a Generation

The numbers as of early 2025 are stark:

Forward P/E: S&P 500 (~21x) vs. STOXX Europe 600 (~14x). Europe trades at a one-third discount.

CAPE Ratio: S&P 500 (~39) vs. MSCI Europe (~21).

An S&P 500 CAPE of 39 is rarefied territory. The only time it significantly crossed 40 was the dot-com bubble. Historically, when a country’s CAPE hits 40, the subsequent 10-year real returns have been negative.

Why Valuation Matters

Valuation is useless for market timing next month, but it is highly predictive over a decade. Robert Shiller’s model currently forecasts average annual nominal returns of 7.8% for European stocks over the next ten years, compared to roughly 5.2% for the U.S.

Meb Faber’s research confirms this: from 1993 to 2018, investing in the cheapest quartile of countries by CAPE returned 3,052%. The S&P 500 returned 962%. Starting price is the primary driver of long-term wealth.

What "Europe" Actually Is

You aren't buying the "European economy." You are buying global businesses headquartered in Europe: Nestlé, ASML, Novo Nordisk, LVMH, and Shell. European indexes provide a different sector mix than the S&P 500. You get less mega-cap tech concentration and more exposure to financials, industrials, healthcare, and consumer staples. You also generally get higher dividend yields.

Leadership Rotates

U.S. stocks have dominated for 15 years. Before that, they underperformed for a decade. This cycle is now the longest and most pronounced since 1970, driven by tech dominance and a strong dollar.

The tide is already shifting. In early 2025, the STOXX Europe 600 posted its best monthly outperformance against the S&P 500 in a decade, alongside record ETF inflows. We don't know the exact timing of the full rotation, but the conditions for a shift - extreme valuation gaps and stretched momentum - are all present.

How to Implement

A global market-cap weight puts roughly 15–20% of equities in developed Europe. That is a solid default. If you want to lean into the valuation gap, you can justify a modest overweight by trimming U.S. exposure.

Keep it simple: Use low-cost index ETFs (expense ratios <0.10%).

Ignore the noise: Currency fluctuations (Euro/Pound vs. Dollar) are real but tend to mean-revert over long periods. For most, unhedged exposure is the right move.

Be patient: Europe may not prove itself on a timeline of the next 6-9 months. It requires the discipline to hold through U.S. outperformance so you are there when the cycle flips. But the "rubber band" of valuations is very stretched and likely to snap back to significant European outperformance soon.

The Bottom Line

Europe belongs in a portfolio because it reduces uncompensated concentration. The S&P 500 is trading near a CAPE of 40; the last time that happened, the next decade was a wash for U.S. investors. You don't need a "heroic" view on Europe - you just need a portfolio that doesn't rely on one country staying on top forever.

Disclosures: ArcVest is a fee-only fiduciary RIA. This is for educational purposes, not individualized advice. Investing involves risk. International investing includes currency and regulatory risks. Past performance does not guarantee future results.