Fiduciary Wealth Management

Low-Fee Investment Management

No Commissions.

No Products to Push.

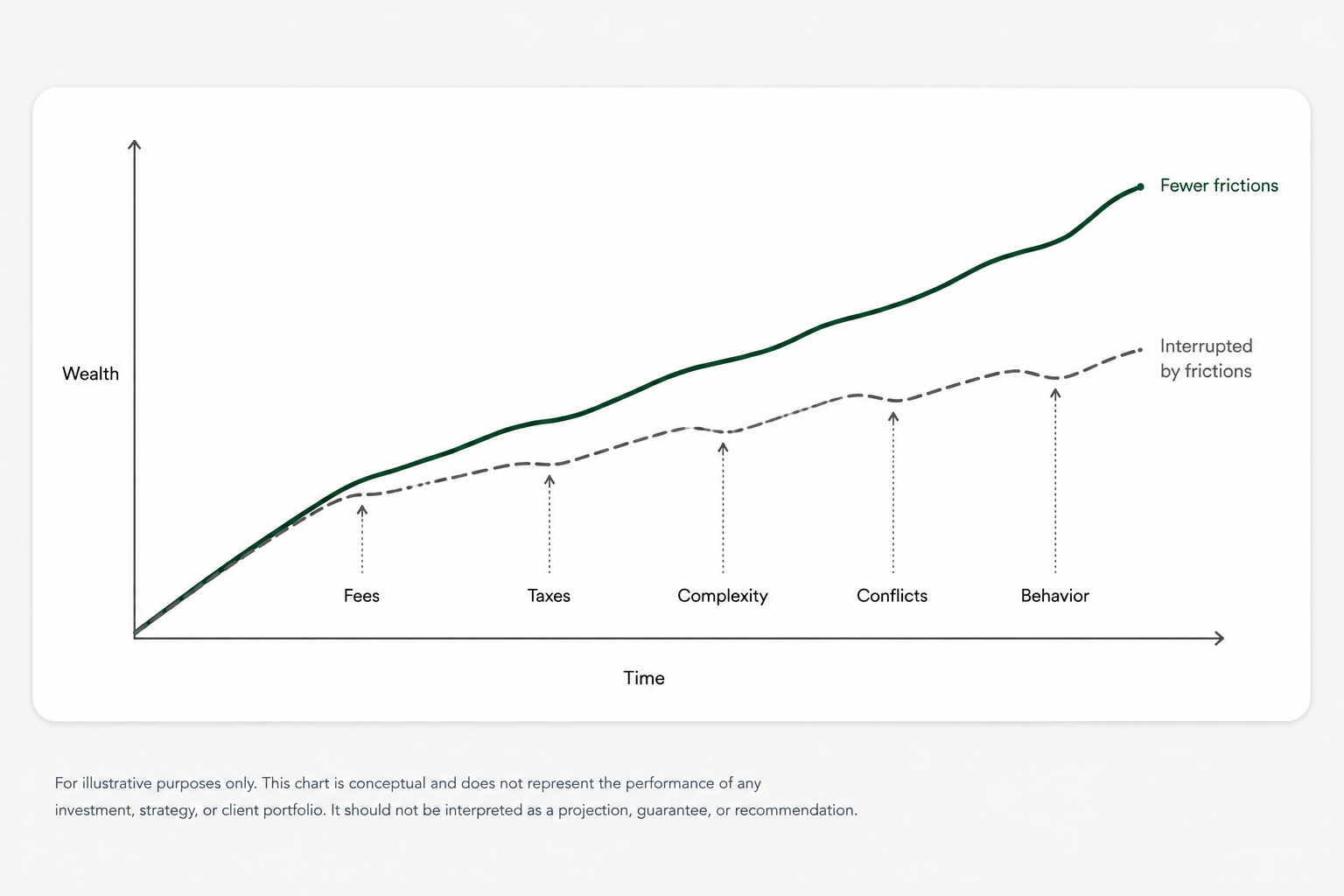

ArcVest is an independent registered investment adviser, or RIA, helping families and institutions build disciplined, low-cost portfolios designed to reduce unnecessary fees, taxes, complexity, and conflicts.

As fiduciaries, we put our clients’ interests first. We use broadly diversified index funds and ETFs, paired with thoughtful planning, tax awareness, and ongoing guidance.

- Evidence-based investing

- Modern tools

- Risk tailored portfolios

- 401(k), IRA, Roth IRA, Trusts, Brokerage

Client Portal View

For illustrative purposes only. Not individualized investment advice or a recommendation. Actual client portfolios may differ. Investing involves risk, including possible loss of principal.

We Help Investors Reduce Friction

Take the step toward a better experience with money.

Sign up to get the Wealth Strategy newsletter with money insights, podcast releases and YouTube videos!

Thank you for subscribing!

Have a great day!

Compound Your Wealth Faster With Lower Fees

ArcVest vs. Wall Street Fee Impact Calculator

See how fee structures alone can affect long-term outcomes when both portfolios earn the same gross return before fees. Adjust the assumptions below to compare the projected ending value, estimated fees, and wealth gap over time.

Portfolio Inputs

Comparison Results

ArcVest

Lower-cost starting assumption

Wall Street

Traditional higher-fee starting assumption

Our Partners:

Why invest with us?

Less Expense

At ArcVest we charge 0.40% of assets under management up to $4MM.

Above $4MM in assets, we charge 0.25%.

There are no start-up fees, no annual administration fees, and no hidden costs.

The Industry

Most wealth managers charge 1% or more of assets that they manage. With so much advancement in technology, that's way too much.

ArcVest has an investment management fee that is a fraction of the national average.

A substantial fee savings keeps more money in your pocket and compounds into greater wealth.

THE FIDUCIARY ADVANTAGE

Working with an advisor that is a fiduciary Registered Investment Advisor (RIA) ensures that your interests are always put first.

This isn’t the case when working with a Wall Street broker adhering to the suitability standard. A broker is under no obligation to put the client’s interest ahead of their own. This generally means higher fee products that benefit themselves and their firm.

RIAs are required by law to put your best interests above all else

How We Work Together

We begin with an extensive discussion of your future needs to create a long-term financial strategy for you and your family.

We develop an Investment Policy Statement (IPS) and then create a cost effective asset allocation model best suited to your goals. We regularly review your progress to ensure you are on the path to meeting your objectives.

Passive Investing

Low Cost Indexing

Accept market returns by buying broadly diversified funds

Rebalance (sell high, buy low) back to Investment Policy Statement (IPS)

Adhere to Efficient Market Hypothesis

*One cannot consistently achieve returns in excess of average market returns on a risk-adjusted basis given the information available. Prices reflect all information.

Investment Philosophy

Clients come first

As an RIA, ArcVest adheres to the fiduciary standard. There are no misaligned incentives, as with broker dealers.

Data-driven philosophy: invest in passive management for better, sustained results

Passive management consistently outperforms active management by all measures

Ignore the noise

Every year investors pay billions of dollars to financial advisors and fund companies who claim they can achieve superior returns. This claim is not supported. Few advisors, if any, have the skills needed to beat the markets, and those few people cannot be identified in advance. Nor does any out-performance persist over time

What do you choose?

There are two options a person can choose when managing an investment portfolio; active management and passive management. Active management is the belief that a person can achieve superior returns over market indexes. In contrast, passive management is all about achieving, as close as possible, the returns of the financial markets. Passive investors understand that market returns are good returns. The desire to beat the market is a powerful force and investors will spend a considerable amount of time and money searching for superior returns. That search is promoted by a multi-billion dollar Wall Street marketing campaign that employs an army of highly compensated salespeople. Despite all the time and money spent trying to identify ways to beat the markets, the net result falls far below expectations.

Low fees deliver value to clients

ArcVest charges 0.25% – 0.40% vs. >1% from most wealth managers. Low fees drive greater client returns.

Customized asset allocation

Truly understand the needs and goals of our clients. Build transparent, liquid and simple portfolios that meet client objectives. Maintain capital discipline through turbulent markets

Listen to those in the know

Every academic study on the subject points to one clear message; in aggregate the more you pay to invest, the lower your returns will be. Our clients do not participate in the massive wealth transfer from Main Street to Wall Street. They earn their fair share of market returns by holding a select basket of low-cost index funds and exchange-traded funds (ETFs) that match market performance.

Do the right thing

After seeing the inner workings of large and boutique investment banks, there is no question low cost investment management is the best method for clients. ArcVest is a leader in low-cost portfolio management. For a small annual fee, we will design, implement and maintain a low-cost, passively managed portfolio that is appropriate for your needs. Our services are economical, efficient and practical

Data trumps hope

Very few mutual funds, hedge funds, private equity funds or investment advisors are able to achieve superior performance with enough consistency to make it worth the effort. After paying fund fees, advisor fees, taxes, broker commissions and other related investment costs, an investor’s return typically falls well below the market. Spending time and money trying to beat the market with active management is counterproductive.

Retirement Calculator

Adjust the inputs — projections update instantly.