Articles

The “Tax Alpha” Hype Cycle: A Reality Check on Direct Indexing

If you’ve spoken to a private wealth manager in the last 18 months, you’ve almost certainly heard the pitch for Direct Indexing.

It is the hottest product in the advisor toolkit right now. The sales pitch is seductive: Why simply buy the S&P 500 when you can own the underlying stocks directly, harvest losses daily, and generate "Tax Alpha" that pays for our fees?

It sounds like a no-brainer. And because it sounds so good, the industry is selling it aggressively.

The Growth Context: Just how aggressive is this push? In 2015, Direct Indexing had $100 billion in assets. By 2020, that had more than tripled to over $350 billion. By June 2025, that number is estimated to have almost tripled again, to roughly $1 trillion by June 2025.

While that is still a fraction of the multi-trillion-dollar high-net-worth market, it is growing at a 10x in 10 years! That’s one of the fastest growing areas of the financial industry. If it feels like everyone is pitching you this, it’s because they are.

So how good is this product anyway?

We dug into the serious research from Vanguard, AQR, and our own internal testing to answer one question: Is the "Tax Alpha" real, or is it just a clever way to justify higher fees?

The short answer: It’s real, but it’s probably half of what you’re being promised.

The Mechanism: What You Are Actually Buying

In a standard S&P 500 ETF, you hold one position. You only get a tax loss if the entire index goes down.

In a Direct Indexing account, you hold hundreds of individual stocks. Even in a year where the S&P 500 is up 20%, some individual stocks (like a Tesla or a Pfizer) might be down. Direct indexing software automatically sells those losers to bank a tax loss, then immediately buys a correlated replacement to keep your exposure steady.

This generates a "bank" of capital losses you can use to offset capital gains elsewhere in your life.

The Data: The Realistic “Tax Alpha” Range

Marketing decks often flaunt potential tax benefits of 100+ basis points (1%+) per year. The independent research paints a much more modest picture.

1. Vanguard: The "Ossification" Problem Vanguard’s research highlights a critical concept called "Ossification." When you first fund the account, everything is fresh. You have plenty of opportunities to harvest losses. But as the market rises over 5–10 years, your portfolio’s cost basis drops. Eventually, most of your positions are sitting on massive unrealized gains. You can’t harvest a loss on a stock you bought at $100 that is now trading at $300, even if it drops to $250.

Vanguard’s bottom line: The benefit isn’t perpetual. In a representative case study, they estimated the long-term annualized benefit on the taxable equity sleeve to be roughly 0.47% (47 bps).

2. AQR: Cash Flows are King AQR’s research adds a critical nuance: The benefit depends entirely on your cash flow. If you just deposit a lump sum and let it sit (Buy and Hold), the tax benefit decays rapidly due to the ossification mentioned above. However, if you are constantly adding new money (creating fresh tax lots with higher basis) or have consistent outside capital gains to offset, the value stays higher for longer.

The ArcVest Verdict

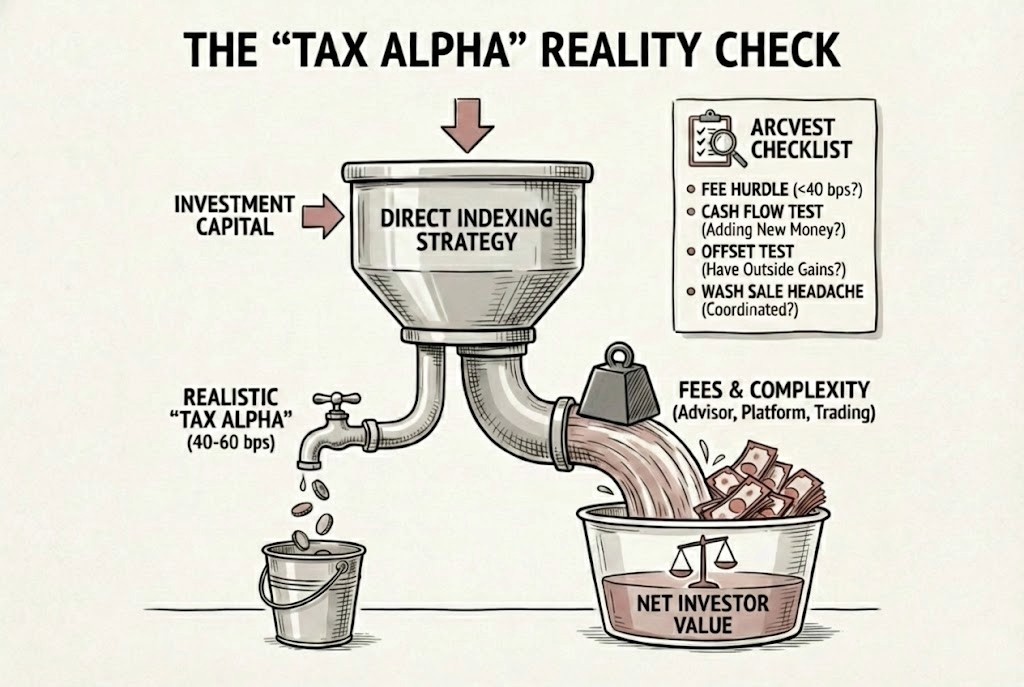

Putting the Vanguard and AQR data together with our own internal testing, we believe high-net-worth investors should underwrite a realistic benefit of 40–60 basis points (0.40% – 0.60%).

~60 bps/year: If you are in the accumulation phase, adding fresh cash monthly/quarterly, and have outside gains (real estate, business sales, hedge fund K-1s) to offset.

~40 bps/year: If you are a "mature" investor with a static portfolio and limited new contributions.

The "Is It Worth It?" Checklist

Here is the uncomfortable truth the industry often ignores: Tax Alpha is a net game.

If a Direct Indexing product generates 50 bps of tax benefit, but the total added cost (advisor fee + platform fee + trading spread) is 60 bps, you have effectively paid 10 bps for the privilege of a more complicated tax return.

Before you sign up, run this simple ArcVest checklist:

The Fee Hurdle: Can you get the all-in cost of the strategy for under 40 bps? (If the fee is higher than the floor of the expected benefit, walk away).

The Cash Flow Test: Will you be adding meaningful new capital to this account every year?

The Offset Test: Do you actually have realized capital gains elsewhere to offset? (Harvesting losses is useless if you don’t have gains to cancel out).

The Wash Sale Headache: Is your advisor coordinating this across all your accounts (including your spouse’s and IRAs)? If not, you risk triggering wash sales that nullify the benefit.

Bottom Line

Direct Indexing is a legitimate tool, not a scam. But it is not magic.

If you can access it for low fees and you fit the profile of an active accumulator with outside gains, it can add ~0.50% of after-tax value to your portfolio. That is meaningful money on a $5M portfolio.

But if you are paying high fees for a static, buy-and-hold portfolio, you are likely better off in a simple, low-cost ETF. Don’t let the tax tail wag the investment dog.

Disclosure: This is educational information, not individualized tax or investment advice. Tax rules are complex and outcomes depend on your full household situation. Consult your CPA/tax advisor for implementation details.

ArcVest

A fiduciary on your side.

Quick links

Support

Copyright 2026. ArcVest. All rights reserved.