Articles

The Math Most Wealth Management Firms Hope You Don’t Run

Do you know what you’re paying for wealth management?

Not the line item on your statement.

Not the number your advisor casually mentions in a review meeting.

I mean the real cost.

Because when it comes to fees, the number itself is rarely what matters most.

It’s what that number becomes over time.

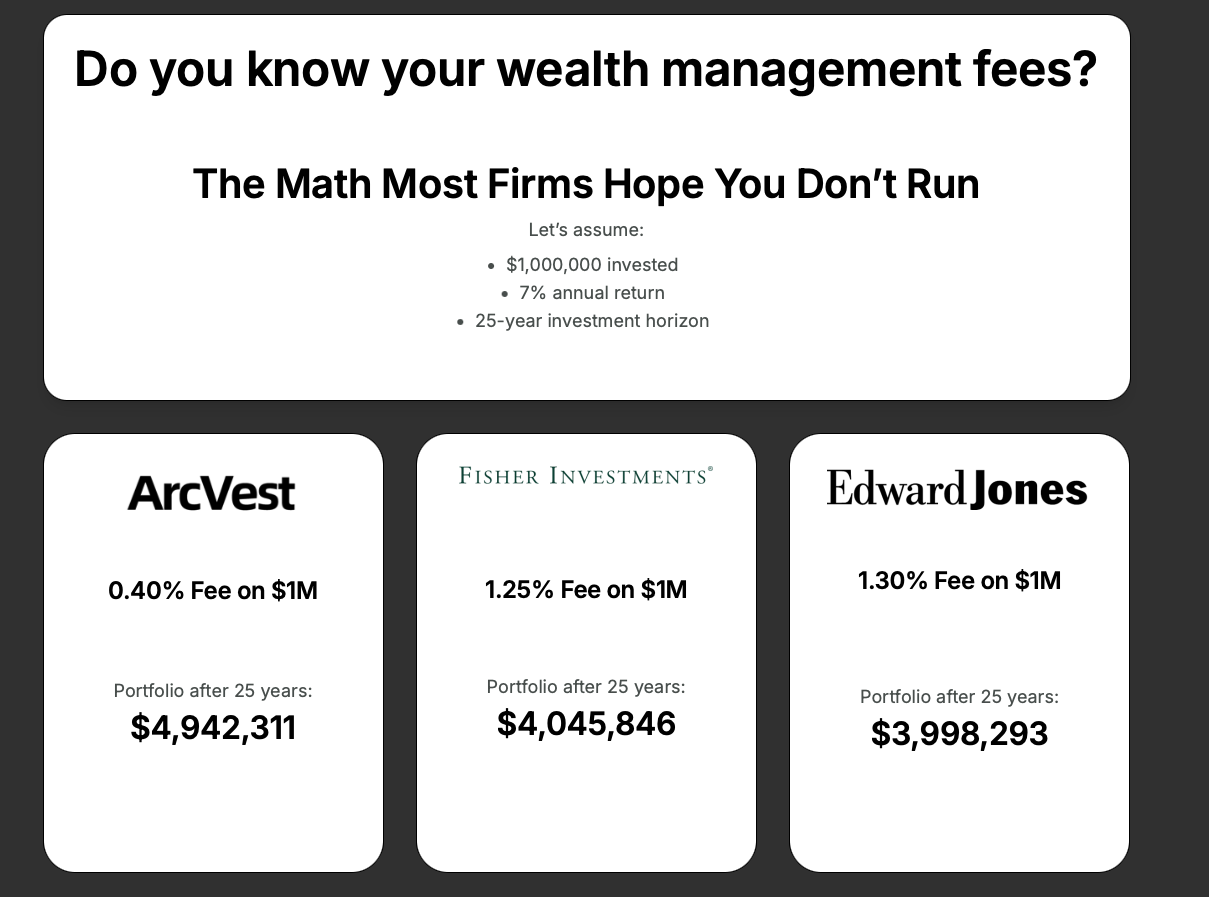

Let’s run a simple example.

$1,000,000 invested

7% annual return

25-year time horizon

No tricks. No exotic assumptions. Just long-term market-level returns over a full investing lifetime.

Now let’s change one variable: the advisory fee.

The Quiet Compounding of Fees

If you pay:

0.40% per year

1.25% per year

1.30% per year

Those percentages don’t look dramatically different. They’re all “around 1%,” right?

But here’s what happens over 25 years.

At 0.40%, your portfolio grows to:

$4,942,311

At 1.25%, your portfolio grows to:

$4,045,846

At 1.30%, your portfolio grows to:

$3,998,293

That’s not a rounding error.

That’s nearly a $1 million difference.

Same markets. Same starting amount. Same return assumption.

The only difference is fees.

And the gap doesn’t happen because someone charges you a big upfront check. It happens quietly. Gradually. Invisibly.

That’s the real power of compounding.

And unfortunately, it works both ways.

Fees Compound Against You

Most investors understand the concept of compounding returns. Few understand the compounding of fees.

When you pay 1.25% instead of 0.40%, you’re not just paying an extra 0.85% per year.

You’re paying:

The fee

The growth that fee would have earned

The growth on that growth

And the growth on that growth

For 25 years.

Fees don’t just reduce returns.

They reduce the capital base that generates future returns.

That’s why small percentages create massive long-term consequences.

And that’s why this math is rarely emphasized in traditional wealth management conversations.

Why High Fees Persist

If the math is this obvious, why do so many firms still charge 1% to 1.5%?

Because:

Most investors anchor to annual percentages.

The dollar impact feels abstract.

The industry has normalized it.

For decades, “1% AUM” became the default pricing model. It was repeated often enough that it stopped being questioned.

But the industry structure hasn’t stood still.

Custody is cheaper.

Trading is cheaper.

Portfolio construction is cheaper.

Technology is dramatically cheaper.

The cost to deliver high-quality investment management has fallen.

Yet many firms still price as if it’s 1998.

The question isn’t whether advisors deserve to be paid.

They do.

The question is: how much of your long-term compounding should you give up for the service you’re receiving?

The Hidden Opportunity Cost

Let’s make this more tangible.

The difference between $4.94 million and $3.99 million is about $944,000.

What does $944,000 represent?

Years of additional retirement income

Legacy capital for children or grandchildren

Philanthropic flexibility

Reduced stress about outliving your money

More optionality in your life

That’s the opportunity cost of ignoring fees.

And here’s the part that’s uncomfortable: the higher-fee portfolio doesn’t need to “fail” for this damage to occur.

It can perform perfectly fine.

It can hit 7% gross returns.

It can look good on paper.

And it still leaves you nearly a million dollars behind.

That’s the silent tax of excessive advisory fees.

“But Don’t You Get What You Pay For?”

This is where the conversation usually shifts.

“Higher fees mean better management.”

“Higher fees mean more sophisticated strategies.”

“Higher fees mean better outcomes.”

But decades of academic research tell a different story.

Markets are highly competitive.

Outperformance is rare and inconsistent.

After fees, the odds are even worse.

So if higher fees don’t reliably produce higher returns, what are you paying for?

Often, you’re paying for:

Brand marketing

Large overhead structures

Layered investment products

Multiple fee stacks (advisor fee + fund expense ratios + trading spreads)

And sometimes, you’re paying for complexity that feels sophisticated but doesn’t meaningfully improve outcomes.

There is a difference between value and cost.

The goal isn’t to pay nothing.

The goal is to pay appropriately.

What Lower Fees Actually Do

Lower fees don’t just increase your ending portfolio value.

They change the math of your life.

They improve:

Sustainable withdrawal rates in retirement

Downside resilience during bear markets

Flexibility around taxes

Probability of meeting long-term goals

If your portfolio earns 7% and you pay 1.30%, your net is 5.70%.

If you pay 0.40%, your net is 6.60%.

That 0.90% spread may sound small. But in a retirement drawdown phase, that difference materially changes how long your money lasts.

Lower fees increase margin of safety.

And margin of safety is what makes financial plans durable.

The Behavioral Side of Fees

There’s another reason this matters.

High fees create pressure.

If you’re paying 1.25% or 1.30%, you subconsciously expect “outperformance.”

You expect action.

You expect complexity.

That pressure can lead advisors to:

Trade more

Add products

Tilt toward narratives

Reach for yield

Layer on alternatives

Not necessarily because it improves outcomes.

But because it justifies the fee.

Lower-cost structures reduce that incentive distortion.

They allow the advisor to focus on what actually works:

Discipline

Diversification

Tax efficiency

Long-term planning

Behavior coaching

The boring stuff.

The stuff that compounds.

This Isn’t About Beating Anyone

This isn’t a criticism of any specific firm.

It’s about math.

If you’re paying over 1%, you deserve to know what that means in dollar terms.

Not annually.

Over decades.

Because wealth management isn’t a one-year decision.

It’s a multi-decade compounding decision.

And the compounding of fees is one of the few variables you can control.

You can’t control markets.

You can’t control inflation.

You can’t control geopolitics.

But you can control costs.

A Better Question to Ask

Instead of asking:

“What is my advisor’s fee?”

Ask:

“What will this fee cost me over 20–30 years?”

Run the numbers.

Use realistic assumptions.

Look at the ending values side by side.

If the difference doesn’t matter to you, that’s fine.

But most investors, when they see nearly a million dollars of difference, pause.

They realize that percentages aren’t small.

They’re exponential.

The ArcVest Approach

At ArcVest, we charge 0.40% on the first $1 million because we believe modern portfolio management should reflect modern economics.

We believe:

Investment management should be efficient.

Technology should reduce costs, not inflate margins.

Clients should keep more of what markets deliver.

Our job isn’t to extract maximum revenue.

It’s to help clients maximize probability of success.

If markets deliver 7%, our goal is simple:

Let you keep as much of that 7% as possible.

Because over 25 years, that difference is life-changing.

Final Thought

Wealth management fees don’t feel urgent.

They don’t make headlines.

They don’t trigger fear.

But they quietly shape outcomes.

The math is simple.

$1,000,000

7% return

25 years

0.40% fee: $4,942,311

1.30% fee: $3,998,293

Nearly a million dollars.

Same market.

Different fee.

That’s not marketing.

That’s compounding.

ArcVest

A fiduciary on your side.

Quick links

Support

Copyright 2026. ArcVest. All rights reserved.