Articles

Evidence-Based Investing

Evidence Over Opinion: The Passive Implementation of Active Choices

Some people hear "passive investing" and think we're not doing anything. I have spoken to folks that say - "well I can do that!" And they are right to a degree. But we don't just buy index funds for our clients and go home.

We use passive tools. The decision about what to own, how much to own, and why - that's the active part. And the evidence shows it's the only part that actually matters.

The financial industry spends enormous energy convincing you that stock-picking and market-timing are the hard problems. They aren't. The hard problem is architecture: how do you assemble a portfolio that captures the global economy's returns without paying someone 1 - 2% a year to flip coins with your retirement?

At ArcVest we replace gut feelings with sixty years of peer-reviewed data. We use broad, low-cost ETFs because the evidence shows they beat high-fee active funds roughly 90% of the time over long horizons. But we don't just buy "the market" and walk away. We apply a logical filter to decide what belongs in your portfolio and what doesn't.

Let's dig in to how that works.

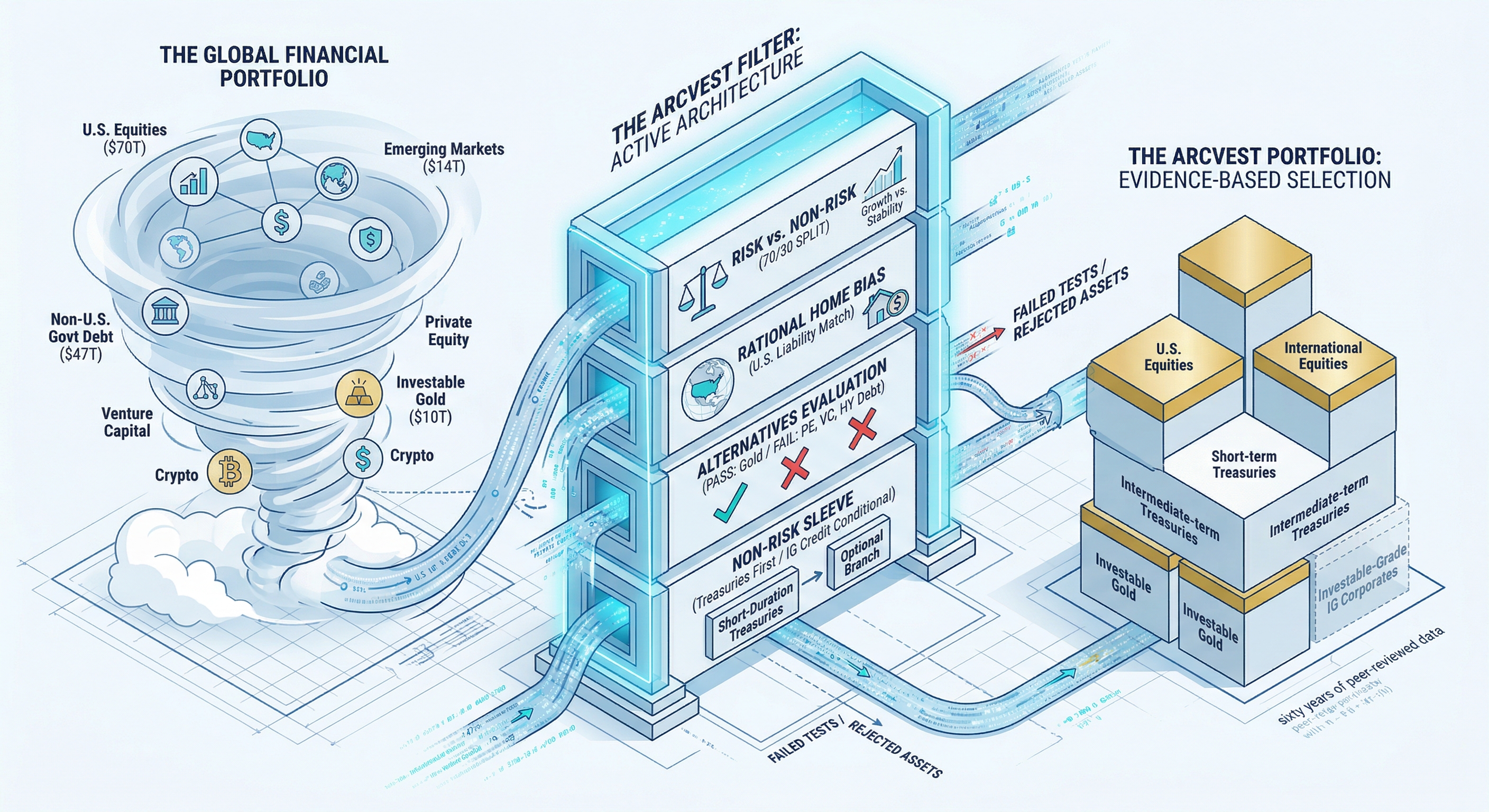

The Starting Point: The Global Financial Portfolio

Every evidence-based investor needs a benchmark. Ours is the aggregate portfolio of every investable dollar on Earth. We built this from SIFMA, MSCI, and other detailed sources. Here's what the world actually owns:

Note: U.S. non-Treasury IG debt includes investment-grade corporate bonds (~$9.6T), mortgage-backed securities, agency debt, municipal bonds, and asset-backed securities. IG/HY split estimated from SIFMA and ICE BofA data. ArcVest weights shown as ranges reflect client-specific allocation.

Note: If you count all gold ever mined (~$24.3T), gold's world weight rises to 7.9%. Under that broader lens, ArcVest's 7% position is slightly underweight.

Look at the ArcVest column. It's mostly zeros. That's the point. We don't buy the world portfolio. We run it through a filter and keep only what survives.

The Filter: Four Decisions That Build Your Portfolio

Every dollar in your portfolio passed four tests. If it failed any one of them, it's out. The numbers presented in this article walk through a typical implementation, although an actual implementation will vary by client.

1. Risk vs. Non-Risk

Over the last century, 100% equities has been the mathematically correct answer. But you aren't a spreadsheet. Most people cannot sit through a 50% drawdown without selling at the bottom and locking in permanent losses. Behavior is the biggest risk in your portfolio, not volatility.

We start with a 70% risk / 30% non-risk split. The 70% is your growth engine. The 30% is your parachute - the thing that lets you hold the 70% when markets go haywire.

2. The Equity Engine

Within that 70%, we hold roughly 2/3 U.S. and 1/3 international. Purists argue for a market-cap-weighted 40% international allocation. We don't.

Your mortgage, your taxes, your grocery bills, your Social Security - all denominated in dollars. You have real U.S. liabilities. Your portfolio should reflect that. We call this "Rational Home Bias." We diversify globally to capture growth outside the U.S., but we don't pretend you live in a currency-neutral vacuum.

3. Alternatives: Keep Gold, Kill Everything Else

This is where most advisors load up on expensive garbage. We go the other direction.

Gold passes. It's a proven store of value with near-zero correlation to equities. When stocks collapse, gold tends to hold or rise. That's the behavior you want from a diversifier. It earns its seat.

Private equity, venture capital, and private credit fail. Not because the managers or underlying assets are bad, but because the fee structures destroy the returns before they reach you. PE and VC funds typically charge 4 - 7% per year in total costs. The academic evidence on PE alpha after fees is damning - for most investors, there is none. The "No"isthe alpha.

High-yield corporate bonds fail. High-yield debt is equity risk dressed up in a bond wrapper. You take on meaningful default risk, you get equity-like drawdowns in a crisis, and you give up the upside that actual equities provide. If you want risk, own stocks. At least you get compensated with uncapped upside. High yield gives you capped upside with uncapped downside. We rarely hold it.

Investment-grade corporate credit passes - conditionally. IG corporates are a different animal. You're lending to Apple, Microsoft, Johnson & Johnson - companies with balance sheets stronger than most countries. The default risk is near zero. The spread over Treasuries is modest, but it's real income with manageable risk. For clients where the additional yield improves their plan, we hold IG credit as part of the non-risk sleeve. For clients who don't need it, we keep the full allocation in Treasuries.

4. The Non-Risk Sleeve: Treasuries First, Credit When It Earns It

The global bond market has an average maturity of roughly 13 years. That's a massive bet on interest rates. We don't make that bet.

Our non-risk allocation anchors in short-duration U.S. Treasuries - the 0 to 3-year zone. These have one job: be there when you need them. They aren't a profit center. They're a shock absorber. We keep them short so they do that job without exposing you to rate risk you aren't being paid to take.

For clients whose financial plans benefit from additional yield, we add investment-grade corporate bonds alongside Treasuries. The mix between Treasuries and IG credit shifts based on the client's specific needs - anywhere from 100% Treasuries to a blend that includes up to 30% in IG corporates. What almost never changes: we don't reach for yield by going down in credit quality.

Tactical Tilts: We Watch the Data

Evidence-based doesn't mean static. We monitor conditions and adjust when the data justifies it.

Equity geography. If U.S. valuations stretch to levels where forward returns look meaningfully impaired, we increase our international allocation. We're already shifting slightly for some clients.

Duration. We stay short by default. We'll extend only if the term premium - the extra yield the market pays for holding longer bonds - becomes compelling enough to justify the added risk. Right now it doesn't.

Credit. We hold investment-grade corporates when spreads justify the incremental risk over Treasuries. When IG spreads are tight - as they are today - the extra yield barely compensates for the added complexity. When spreads widen, IG credit becomes a genuine source of return. We adjust accordingly.

Everything else. The bar for adding any new asset class is high: it must be liquid, cheap, transparent, and backed by evidence that it improves risk-adjusted returns after fees. Almost nothing clears that bar.

The Bottom Line

We own six things. U.S. stocks, international stocks, short-term Treasuries, intermediate-term Treasuries, investment-grade corporate bonds, and gold. Each one passed every test. Everything else failed at least one.

The financial industry makes its money by making this complicated. We make ours by keeping it simple and keeping you in your seat. Your behavior - not your fund selection, not your stock picks - is the single largest determinant of your lifetime investment returns.

Passive instruments. Active architecture. That's the ArcVest way.

ArcVest is a fee-only fiduciary registered investment adviser. This article is for educational purposes and does not constitute personalized investment, tax, or legal advice. Investing involves risk, including the potential loss of principal. Past performance does not guarantee future results.

ArcVest

A fiduciary on your side.

Quick links

Support

Copyright 2026. ArcVest. All rights reserved.