Articles

Time to Increase International Exposure

The Spring Is Coiled

Diversification has been painful. For fifteen years, owning anything outside the S&P 500 felt like a tax on your portfolio. International developed stocks lagged. Emerging markets went sideways. Your neighbor who put everything in a Nasdaq ETF looked like a genius.

This is what diversification looks like some times.

If diversification felt good every single year, everyone would do it. It would stop working. The discomfort is the source of the return premium. The crowd abandons what hurts. And then the math catches up.

The math is about to catch up.

The Numbers

Let's start with what you're paying for US stocks right now.

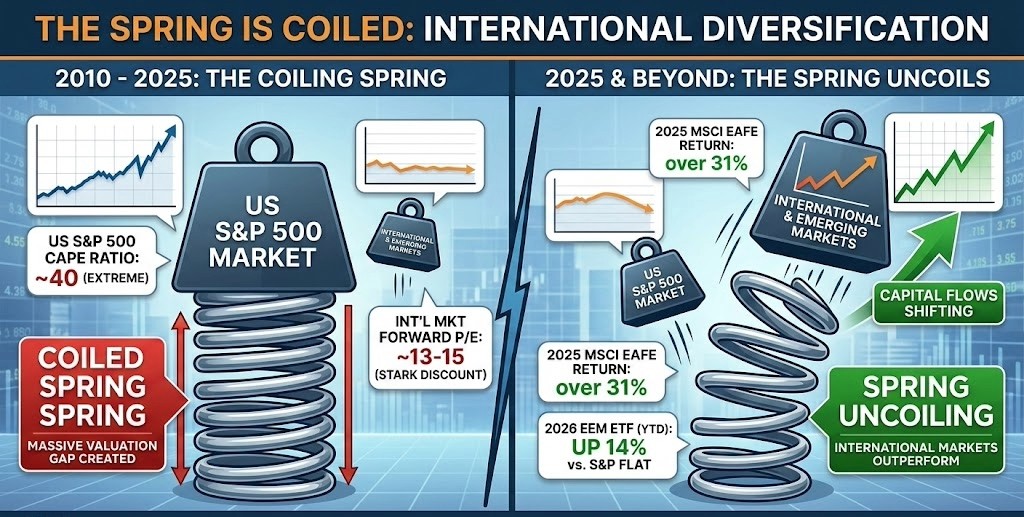

The S&P 500's Shiller CAPE ratio sits at roughly 40. That's nearly 2.5 times the long-term median of 17. The only other time this ratio exceeded 40 was the dot-com bubble. On a forward price-to-earnings basis, the S&P 500 trades at about 22 times next year's earnings. The 10-year average is 18.7.

Now look outside the US.

Developed international stocks (the MSCI EAFE Index) trade at roughly 15 times forward earnings. Close to their 10-year average of 14.5. Emerging market stocks trade at about 13 times forward earnings. Every single sector in the EAFE index trades at a discount to its US counterpart. Every one.

Read those numbers again. You're paying 22 times earnings for US stocks and 13 times earnings for emerging market stocks. That's a 40% discount. Research Affiliates puts it more starkly: across five different valuation metrics, developed international markets are 37% to 46% cheaper than the US. Emerging markets are 40% to 60% cheaper. The spread has rarely been wider.

That gap is the coiled spring.

Why the Gap Exists

Two things drove US outperformance over the past fifteen years. Both are running out of road.

First, US corporate profit margins expanded for a decade straight. About 60% of that expansion came from two tailwinds: falling interest rates and globalization. Interest rates are no longer falling. Globalization is in reverse. The structural forces that inflated margins are no longer tailwinds.

Second, investors bid up the multiples they were willing to pay. The S&P 500's earnings multiple expanded from reasonable levels in 2012 to historically extreme levels today. Meanwhile, emerging market earnings in nominal dollar terms haven't grown in fifteen years. Emerging market CAPE ratios went up through 2012, then collapsed back to where they started. The US went the other direction.

Those two trends - margin expansion and multiple expansion - are arithmetic, not magic. They don't compound forever. They reverse.

What Happens When the Spring Uncoils

This is where CAPE earns its keep.

Robert Shiller's cyclically adjusted P/E ratio uses ten years of inflation-adjusted earnings to smooth out business cycles. The measure isn't perfect for timing. Over one to three years, momentum and narrative drive stocks more than valuation. But over seven to fifteen years, the relationship between starting CAPE and subsequent returns is one of the most reliable patterns in financial markets.

The data is clean: the S&P 500 has never delivered annualized returns above 10% when starting from a CAPE above 25. Every period of sub-5% annualized returns started with a CAPE above 30. The current CAPE is 40.

The major investment firms are reaching similar conclusions. Morningstar surveyed the 2026 capital market assumptions from Schwab, Research Affiliates, GMO, and others. The consensus range for US large cap nominal returns over the next decade runs from 3% to 6%. For developed international stocks, the range is 7% to 8%. For emerging markets, 7.5% to 10%.

GMO, which has the most bearish US outlook, projects negative 6% real returns for US large caps over seven years. Their emerging market value forecast is positive 3.8% real.

These aren't fringe analysts. This is mainstream institutional research, all pointing the same direction.

The Price of Certainty

Here's the part that keeps people stuck.

US stocks feel safe. You know the companies. You use their products. They've made you money for fifteen years. International stocks feel risky. You don't follow European banks or Korean semiconductor firms. The headlines from emerging markets involve trade disputes and political risk and war.

That familiarity premium has a price. Right now, you're paying roughly 60% more per dollar of earnings for the comfort of owning US stocks instead of emerging market stocks. The question isn't whether US companies are great. They are. The question is whether they're great enough to justify paying double the earnings multiple of their international peers.

In 2025, the answer started to shift. The MSCI EAFE index returned over 31%. Emerging markets outperformed the S&P 500 by 2x. Year-to-date 2026, iShares MSCI Emerging Markets ETF (EEM) is up 14% while the S&P 500 is effectively flat. The is dollar weakening, and capital is starting to flow out of US assets and into foreign markets.

None of this guarantees continued outperformance. But the valuation gap doesn't close overnight. It took fifteen years to build. The unwind will take years, too. The question is whether you'll be positioned for it or watching from the sidelines.

The ArcVest Take

Diversification isn't supposed to feel comfortable. The last fifteen years proved that. If it were easy to hold international stocks while US stocks soared, everyone would have done it. The payoff from diversification comes from bearing the discomfort that other investors refuse to bear.

The valuation data says the spring is coiled. US stocks are priced to deliver mid-single-digit returns for a decade. International and emerging market stocks are priced to deliver meaningfully more. The two biggest tailwinds behind US outperformance — falling rates and globalization — have stalled.

You don't need to predict which year the turn happens. You need to be positioned before it does.

ArcVest is a registered investment adviser. The information presented is for educational and informational purposes only and should not be construed as specific investment, accounting, legal, or tax advice. This content does not constitute an offer or a solicitation to buy or sell any specific securities, investments, or investment strategies. All investments involve risk, including the potential for loss of principal. Past performance is not a guarantee of future results. Please consult with a qualified financial, tax, or legal professional regarding your specific situation before implementing any strategy discussed herein.

ArcVest

A fiduciary on your side.

Quick links

Support

Copyright 2026. ArcVest. All rights reserved.